Vermont: First out of the gate with preliminary 2027 ACA rate filings: up 6.5% on average

Thu, 05/28/2026 - 3:22pm

Every year around this time I start my annual individual & small group market rate filing analysis project. This involves spending months painstakingly tracking every insurance carrier rate filing for the upcoming year to determine just how much average insurance policy premiums on the individual market are projected to change.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier:

- How many effectuated enrollees they have in ACA-compliant policies this year;

- The average projected rate change for those policies;

- Ideally, a breakout of the reasons behind the changes.

Usually the reasons given are fairly vague things like "increased morbidity" (ie, a sicker risk pool) or the like. Sometimes, however, there's a very specific reason given for some or all of the premium changes. Major examples of this include:

- 2017: 2 of the 3 "training wheel" programs included in the original ACA legislation expired (federal reinsurance and risk corridors)

- 2018: Trump 1.0 cut off Cost Sharing Reduction CSR) reimbursement payments to carriers

- 2021: Accounting for the impact of the COVID-19 pandemic on health insurance claims

And of course, for 2026...

- The expiration of the upgraded premium subsidies introduced by the American Rescue Plan Act in 2021, which were extended by the Inflation Reduction Act through the end of 2025.

This upgrade finally brought the ACA's premium tax credits up to the levels they should have been in the first place while also removing the hated "subsidy cliff" which caused households which earn even $1 more than 400% of the Federal Poverty Level to lose eligibility to any federal subsidies at all.

Unfortunately, both of these improvements expired at the end of 2025, resulting in gross ACA premiums shooting up nearly 20% and net ACA premiums jumping an astonishing 58% on average this year.

It has also resulted in at least 3 million ACA enrollees already losing healthcare coverage as of April (and likely far more than that before the end of this year).

Well, it's May now, which means that it's time to dust off my spreadsheet and start digging through SERFF (System for Electronic Rates & Form Filing) databases and state insurance dept. websites again to see what the actuaries crunching numbers at hundreds of health insurance carriers around the country have come up with for the 2027 Open Enrollment Period.

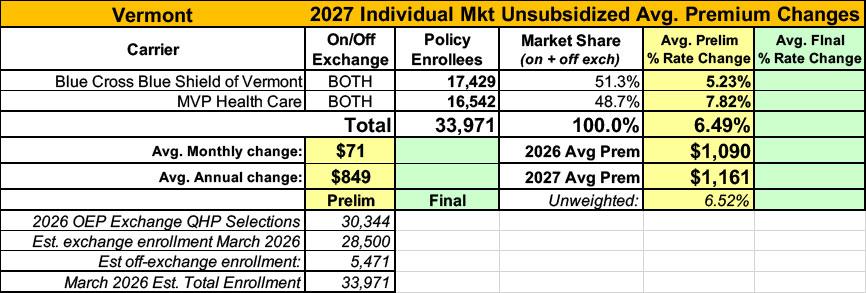

This is a months-long process which includes preliminary filings, reviews by state regulators, revisions to the filings and final approval. Different states have different timeframes for when they get the ball rolling, but the first states to do so generally include Vermont, Washington, Oregon, Maryland & New York...and sure enough, VERMONT has indeed published the preliminary filings for both of their individual and small group market carriers (Blue Cross Blue Shield of VT and MVP Health Care).

So, with that, let's take a look...

BLUE CROSS BLUE SHIELD OF VERMONT 2027 VERMONT QHP MARKET RATE FILINGS ACTUARIAL MEMORANDUM

1.4. Proposed Rate Change(s)

1.4.1. Individual Market

The average rate change is 5.2 percent. Changes for specific plans range from 1.6 percent to 10.8 percent. The range of changes is due to changes to the actuarial values and plan designs.

1.4.2. Small Group Market

The average rate change is 3.1 percent. Changes for specific plans range from -0.3 percent to 4.6 percent. The range of changes is due to changes to the actuarial values and plan designs.

1.5. Reason for Rate Change(s)

The starting point of any rate analysis is an assessment of actual to expected experience results. The Blue Cross VT 2026 Vermont QHP Market Filings (2026 filings, BCVT-134524605, BCVT-134524673) used calendar year 2024 claims as its basis. We first update the baseline for this rate filing to actual calendar year 2025 (CY 2025) experience projected to 2027, as described in detail in this Actuarial Memorandum. In these markets, an update to the experience includes the restatement of claims, pharmacy rebates, and risk adjustment. There were two one-time events in 2025 that resulted in lower claims: (1)); the mid-year cost reductions at two Vermont hospitals and (2) the introduction of a biosimilar for Stelara.

...Trend continues to be one of the main drivers of the change in rates. The 2026 approved rates included assumptions for projecting 2025 to 2026 which must be re-examined, and an additional year of projected trend must be applied from 2026 to 2027. Medical unit cost trend for 2025 to 2026 decreased due to lower hospital budgets and Blue Cross VT’s contracting efforts. We also anticipate a continued positive utilization trend for both medical and pharmacy services.

...Blue Cross VT will offer two types (Standard and Non-Standard) of plans to the individual and small group markets in 2027. These plans include coverage for all Essential Health Benefits (EHB). All standard plans, Vermont Select plans, and Vermont Preferred plans are on the Exclusive Provider Organization (EPO) network and offer members access to a nationwide network of providers, including over 97 percent of the providers in Vermont. The Vermont Basic plans, new in 2027, are offered on the VHP Select network, which covers the same Vermont providers as the EPO network, and also includes a select list of providers in neighboring counties in Massachusetts, New York, and New Hampshire.

Blue Cross VT Standard Plans: Blue Cross VT is providing rates for the Standard plans with benefits as approved by the Green Mountain Care Board, which are outlined in Exhibit 1A. The form filing for these products can be found under BCVT-134891366 for deductible plans and BCVT-134891432 for Consumer Driven Health plans (CDHP). Blue Cross VT is also providing rates for the catastrophic plan, also outlined in Exhibit 1A. The form filing for this plan can be found under BCVT-134891439.

Blue Cross VT Non-Standard Plans: Blue Cross VT is providing rates for three non-standard products. The first product, Vermont Select, offers HSA compatible plans with the deductible at the same level as the out-of-pocket. The second product, Vermont Preferred, offers plans with zero cost share for some primary care or mental health visits and some specialist visits to manage diabetes and heart disease. Both products waive deductibles for wellness drugs. The third product, Vermont Basic, is a new suite of products for 2027 and offers lower cost HSA-compatible plans. The details of the benefit structures are outlined in exhibits 1B-IND and 1B-SMG. The form filings for these products can be found under BCVT-134891417 for Vermont Preferred, and BCVT-134891404 for Vermont Select, and BCVT-134891449 for Vermont Basic.

Reflective Silver Plans: Pursuant to Act 88, Blue Cross VT will offer certain silver plans only off-exchange for the individual market for the 2027 plan year. These plans are “reflective” of the Exchange plans, with only a $5 copayment, 5 percent coinsurance or $25 deductible difference from the Exchange plan.

...As of February 2026, Blue Cross VT had 30,609 members enrolled in the Vermont QHP markets, with 17,428 enrolled individually through Vermont Health Connect or directly through Blue Cross VT and 13,181 small group employees and their dependents. We used this information as the starting point to project the 2027 enrollment and the distribution by plan.

For 2027, in the small group market, all reflective plans are terminated, as they are no longer needed with the permanent unmerging of the markets. We mapped all small group members in reflective plans to the equivalent on-exchange silver plans.

As of the information date of this memorandum, the new Vermont Basic products were still under consideration by the GMCB. We therefore do not have membership projected in these products. That said, if we were to project membership, we would not assume an overall change to the mix by metal level from the current enrollment and therefore the impact to all other products premium would be immaterial.

Exhibits 2A-IND and 2A-SMG show the 2027 Blue Cross VT individual and small group projected population by plan and market.

Blue Cross VT expects to cover 209,136 member months in the individual market and 158,172 in the small group market in 2027. We use this projected membership to adjust our Index Rate for demographics, morbidity, benefit changes, and other allowable adjustments described below.

Note: Dividing those numbers by twelve gives 17,428 individual market members and 13,181 in the small group market, which basically means BCBS VT expects their 2027 enrollment to be pretty much the same as it is this year.

Impact of the expiration of the enhanced APTC

We do not expect additional movement out of the individual market due to the expiration of the enhanced subsidies at the end of 2025 beyond the impact captured by the changes in the pool morbidity due to voluntary cancelations (below). This factor is therefore 1.0000.

The full memo is a whopping 31 pages long, but aside from the actual average rate increases and the current effectuated enrollment numbers, the most noteworthy thing I get from this is that Vermont, which used to have a merged individual and small group market, is permanently separating them out (joining every other state except for Massachusetts, I believe).

MVP HEALTH PLAN, INC ACTUARIAL MEMORANDUM: 2027 Vermont Individual Exchange Filing

This memorandum details the methods and assumptions underlying the proposed 2027 premium rates for the State of Vermont’s Individual ACA compliant market. These products will be issued by MVP Health Plan, Inc. (MVP), a non-profit subsidiary of MVP Health Care, Inc. The rate filing has been prepared to satisfy the requirements of 8 V.S.A §5104 as well as the requirements of the Federal ACA including 45 CFR Part 156, §156.80.

The premium rates are effective between 1/1/2027 and 12/31/2027. There are no benefit plans being retired, nor are there any new benefit plans being added. MVP modified several of the benefits being offered, and the updated forms have been submitted in a separate SERFF filing. The proposed average rate increase (MVP’s revenue increase) is 7.8%, with increases ranging from 4.7% to 108.8%.

...Several adjustments to the experience period incurred claim costs were necessary to adjust for items not captured in the experience period. The adjustments are explained below.

Line 11- Adjustment for Full Coverage of Insulin

MVP has made the change to cover diabetic insulin in full on all plans. This was done to align coverage for insulin among the commercial lines of business in both states that MVP operates in. MVP analyzed historic claim data and found that this adjustment is worth $0.38 PMPM.

Line 12- Adjustment for Change in Coverage of Weight Loss GLP-1s

Beginning January 1, 2026, MVP is no longer covering weight loss GLP-1 drugs except for certain medically accepted indications. MVP found, after analyzing the emerging data for the 1st quarter of 2026, that utilization of weight loss GLP-1 drugs has dropped. MVP has therefore reduced the experience period data to only reflect $4 PMPM, which is our best estimate of 2026 expense based on emerging trends and seasonality. This adjustment reduces the premium by $8.71 PMPM. Please note that this is the net impact on claim expense after considering any reduction in manufacturer rebates as a result of this policy change.

Line 13- Adjustment for H.766

Vermont Act 111 (also referred to as House Bill H.766) is “an act relating to prior authorization and step therapy requirements, health insurance claims, and provider contracts,” and it has the potential to significantly raise the cost of medical claims in the Vermont commercial health insurance market. Previous portions of this Act relating to prior authorization requirements went into effect on 1/1/25 so this is already included in the experience period. The portions of the Act which went into effect on 1/1/26 are related to clinical edits for claims.

The actuarial team relied on data performed by our operations team, which identified claim edits from historical claims that would not be allowed under the new regulations. The actuarial team converted the billed costs for those lines to allowed claim expense (by applying the average billed/allowed charge ratio). Using that methodology results in a total claim expense increase of 0.5%, or $4.03 PMPM, and we have used that estimate in this filing. This number was approved in the 2026 rate filings and MVP does not have any new information to revise this assumption, therefore we are continuing to use last year’s estimate.

Line 14- Impact of IRA Subsidy Expiration

The IRA-enhanced Advanced Premium Tax Credit (APTC) subsidies expired at the end of 2025. A disproportionate share of healthy members are expected to leave the market, resulting in increased morbidity. To analyze this, MVP relied on our own internal claim and risk score data. We do not believe the full impact is present in our current 2026 membership figures, as we continue to see retroactive coverage terminations for non-payment of premium.

MVP assumed the lapse of 16% of contracts that receive APTC subsidies and have no hierarchical condition categories (HCCs) and 3.5% of silver and bronze contracts that receive APTC subsidies and have one HCC. The overall disenrollment would be 9.7% of MVP’s total individual market membership. Removing the claims and membership for these members from our population (which simulates these members leaving the market in total) results in a morbidity impact of 5.7%, or $47.88 PMPM.

Line 15- Adjustment for Reduction in High Tech Imaging Prior Auth

MVP terminated an arrangement on April 14, 2025 that performed prior authorization for high tech imaging services through an external vendor. These services were outside of the scope of Act 111 and are not included in the above estimate. The claim impact is expected to be 0.022%, or $0.19 PMPM, which represents the value of imaging services avoided during the time period for which the vendor was in place during the experience period.

Line 16- Adjustment for Act 55

Act 55, also known as H.266, which caps certain prescription drug costs relative to ASP, went into effect on January 1, 2026. MVP analyzed the impact of this change by “re-pricing” 2025 outpatient drug utilization under the new regulations, and we have quantified this impact to be a $35.95 PMPM reduction to premium rates.

Line 17- Adjustment for High Cost Claimants in 2025 Above National Threshold

MVP is expecting recoveries for members with incurred claims in the experience period above the national threshold of $1 million. These recoveries are worth $3.83 PMPM.

Adjustment for S.190

The impact of bill S.190, which is related to reference-based pricing, is not incorporated in our filing. MVP recognizes that the bill would have a significant impact on the cost of hospital care in the state of Vermont, but there is still uncertainty around the scope and parameters of the pricing. If the bill is passed, MVP can provide an estimate of the impact.

Again, I'm sure there's a whole mess of stuff I'm missing, but the big bullet points here are:

- MVP will be fully covering diabetic insulin for all enrollees next year (which will only raise premiums $4.56 per year per enrolle)

- Several new state healthcare regulatory bills have passed regarding prior authorization, step therapy, caps on prescription drug pricing and reference-based pricing

and the big one:

- Unlike BCBS VT, MVP Health says that they expect more negative impact to the risk pool from more enrollees dropping coverage due to the enhanced federal subsidies expiring...to the tune of 9.7% of their enrollees (in fact, this was actually down by 11.5% as of April...but I'm not sure if the 9.7% projection was being compared against their February enrollment data, against the total number who signed up for coverage during Open Enrollment, or what. They're literally baking a 5.7 point increase in 2027 for this factor alone...causing average premiums to jump by nearly $48/month or another $575/year per enrollee.

Since MVP holds around 49% of the market, taken literally this means that the subsidy expiration alone will cause average premiums to go up ~$23.30/mo or ~$280 per enrollee across the full market next year.

Here's what this looks like overall for the VT individual market...a weighted average projected unsubsidized premium increase of around 6.5% across both carriers:

Assuming these rates go through as is (again, there are usually changes to them before the final rates are locked in), it would push average unsubsidized premiums to a whopping $1,161/month per enrollee.

IT'S IMPORTANT TO REITERATE THAT THIS IS FOR UNSUBSIDIZED ENROLLEES ONLY.

While the enhanced subsidies have expired, 77% of Vermont enrollees are still receiving the standard federal subsidies, and around 56% are also eligible for Vermont's supplemental state subsidies.

Meanwhile, the Vermont small group market is looking at a slightly higher percentage rate increase of around 6.8% (unfortunately, I rarely know what the average premiums are for this market):

| Attachment | Size |

|---|---|

| 2.81 MB | |

| 5.04 MB |

Advertisement