How much more are DISTRICT OF COLUMBIA ACA enrollees *really* paying this year due to Trump/GOP policies?

Thu, 05/28/2026 - 12:54pm

IMPORTANT: See the original post in this series for an explanation of the methodology.

Regular readers know that I've been obsessing over the massive increases in both gross as well as net premiums for ACA health insurance policy enrollees being caused by the combination of Congressional Republicans allowing the enhanced federal tax credits to expire as well as other Trump Regime policy changes for well over a year and a half now.

I've written countless analyses of how much both gross and net premiums skyrocketed from 2025 to 2026 across different states, different income levels and various other demographics...and last week it was revealed that over 3 million ACA exchange enrollees had already been priced out of the market as of April, with the number almost certain to climb further throughout the rest of 2026.

As I've repeatedly warned, however, the increases in premium costs (whether gross or net) are only half the story. The other big shoe which is dropping this year is increased out of pocket costs as millions of the ~19.2 million or so remaining enrollees as of April have been forced to downgrade their coverage to avoid (or at least minimize) those massive premium spikes.

In most cases this means moving to plans with higher deductibles, higher co-pays & higher coinsurance costs. In many cases this has also included moving to plans with worse networks, referral requirements to see specialists and so on.

With that in mind, that's exactly what I've decided to set out to do: Calculate the average year over year increase not just in net premiums (that is, how much more ACA enrollees are having to pay each month) but also the year over year change in average out of pocket costs.

Today I'm looking at the DISTRICT OF COLUMBIA:

Before I begin, it's important to keep in mind that in addition to expanding Medicaid to residents who earn up to 138% of the Federal Poverty Level (FPL), DC also has a special "Basic Health Plan" healthcare coverage program in place for residents who earn between 138 - 200% FPL:

Section 1331 of the Affordable Care Act gives states the option of creating a Basic Health Program (BHP), a health benefits coverage program for low-income residents who would otherwise be eligible to purchase coverage through the Health Insurance Marketplace. The Basic Health Program gives states the ability to provide more affordable coverage for these low-income residents and improve continuity of care for people whose income fluctuates above and below Medicaid and Children's Health Insurance Program (CHIP) levels.

Through the Basic Health Program, states can provide coverage to individuals who are citizens or lawfully present non-citizens, who do not qualify for Medicaid, CHIP, or other minimum essential coverage and have income between 133 percent and 200 percent of the federal poverty level (FPL). People who are lawfully present non-citizens who have income that does not exceed 133 percent of FPL but who are unable to qualify for Medicaid due to such non-citizen status, are also eligible to enroll.

Consistent with the statute, benefits will include at least the ten essential health benefits specified in the Affordable Care Act. The monthly premium and cost sharing charged to eligible individuals will not exceed what an eligible individual would have paid if he or she were to receive coverage from a qualified health plan (QHP) through the Marketplace. A state that operates a Basic Health Program will receive federal funding equal to 95 percent of the amount of the premium tax credits and the cost sharing reductions that would have otherwise been provided to (or on behalf of) eligible individuals if these individuals enrolled in QHPs through the Marketplace.

Three other states also have BHP programs in place: Minnesota, New York and Oregon. DC's BHP program actually replaces their prior Medicaid expansion waiver, which provided Medicaid coverage to residents who earn up to 210% FPL.

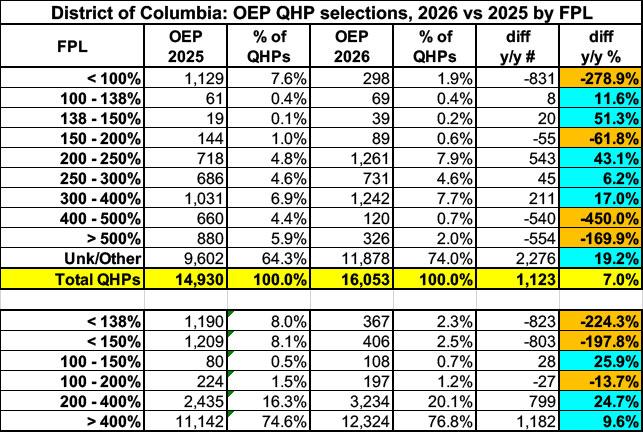

The point is that for both 2025 and 2026, DC has very few ACA exchange enrollees who earn less than 200% FPL.

Nationally, around 65% of all ACA exchange enrollees earn less than 200% FPL. In DC, it was only 9% in 2025, and in 2026 this has dropped further yet to just 3.1%:

This massively skews the other demographics, as you'll see below.

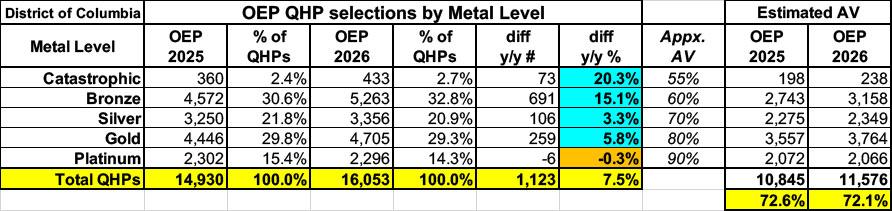

Here's total Open Enrollment plan selections for both 2025 & 2026 broken out by raw metal level:

DC is one of the few states (yes, I'm calling it a state for purposes of this project) where year over year exchange enrollment increased. Part of this is likely due to the shift from the 210% FPL Medicaid cut-off to the 200% FPL BHP cut-off this year; given how few residents are enrolled at all in DC, even a few hundred people makes a big difference (indeed, enrollment in the 200 - 250% range increased by 43% this year).

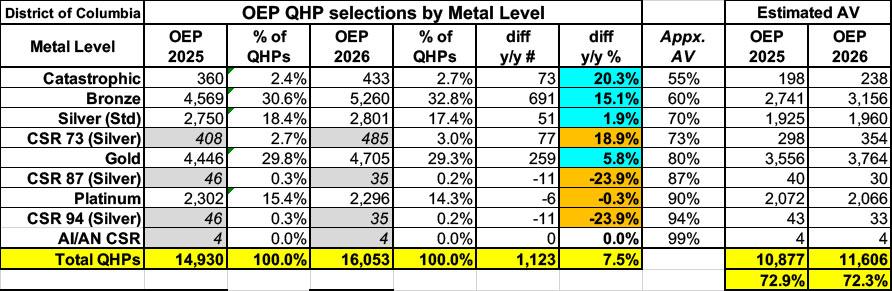

Unlike most of the other states I've analyzed so far, breaking out Silver enrollment into the CSR categories makes almost no difference at all in the average Actuarial Value (AV) of DC enrollees...because there's very few enrollees with CSR to begin with...because the 2 biggest CSR categories are only available to enrollees who earn less than 200% FPL to begin with:

IMPORTANT: I only have detailed CSR category enrollment data for the 30 states hosted via the federal ACA exchange, HealthCare.Gov. Unfortunately, the Centers for Medicare & Medicaid Services (CMS) only provides total CSR enrollment for most of the 21 state-based exchanges (SBEs).

For these states, which includes Connecticut, I'm instead relying on rough estimates based on the percent of enrollees in the 100 - 150%, 150 - 200% and 200 - 250% FPL income brackets who selected Silver plans each year, which can be found in the 2025 & 2026 OEP State, Metal Level, and Enrollment Status Public Use Files (ZIP) from CMS.

These percentages, when converted into raw numbers, correspond fairly closely to the actual CSR category breakouts for FFM states (+ or - 5%), so they should be close enough for my purposes. I've also come up with rough estimates for the AI/AN CSR category based on comparisons of the percent of AI/AN CSR QHPs selected in FFM states to the percent of AI/AN residents within each state. This is less than 3.3% in every SBE state except for New Mexico.

Again, these are broad estimates only but should be reasonably accurate for this project.

Anyway, there's only a small drop in the average AV from 2025 to 2026, from 72.9% to 72.3%.

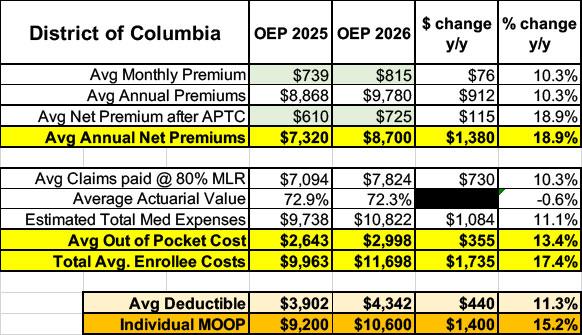

By combining these numbers with the average gross premiums per enrollee I'm able to calculate an estimate of the average total medical expenses each enrollee racks up each year assuming an 80% average Medical Loss Ratio (which, as I stated in the original post, can vary widely by carrier and year, so this should be considered a very broad average only), which looks like so:

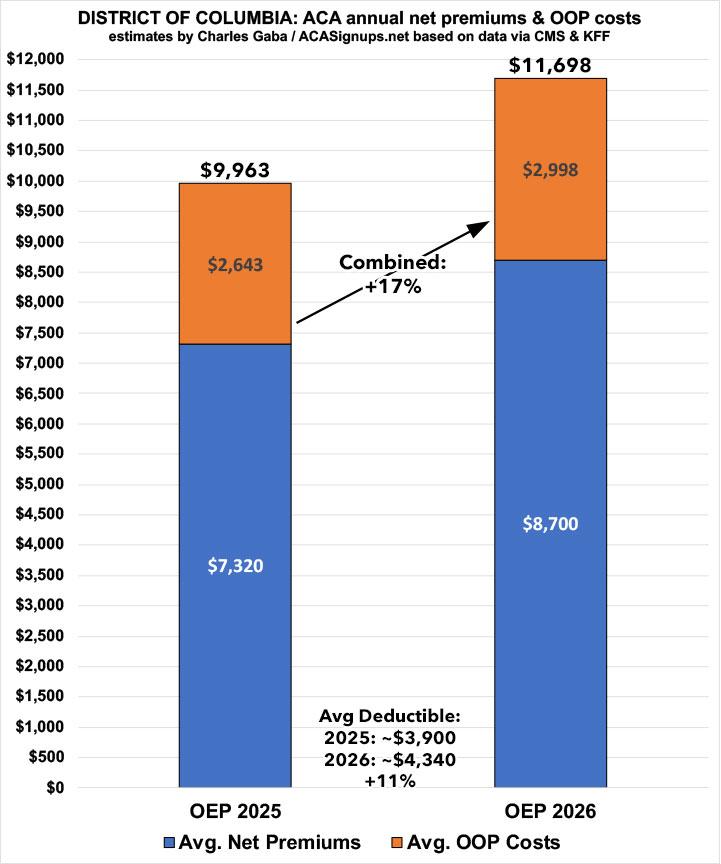

In the District of Columbia, net premiums have gone up around 19% on average. While this is actually at the low end of the scale this year, you have to keep in mind that average net premiums for DC ACA enrollees were already averaging over $7,300 to begin with (again, because well over 90% of them earn more than 200% FPL), so the $1,380 annual bump "only" amounts to a 19% increase.

Meanwhile, average out of pocket expenses "only" increased by around $355/year per enrollee, for a combined average increase of 17.4%...or over $1,700 more per enrollee.

Based on KFF's net data, average deductibles also jumped by ~11% to over $4,300 for single coverage this year, and the maximum (theoretical) out of pocket cut-off for all ACA enrollees went up by over 15% this years to $10,600 for single coverage.

Next up: FLORIDA.

Advertisement